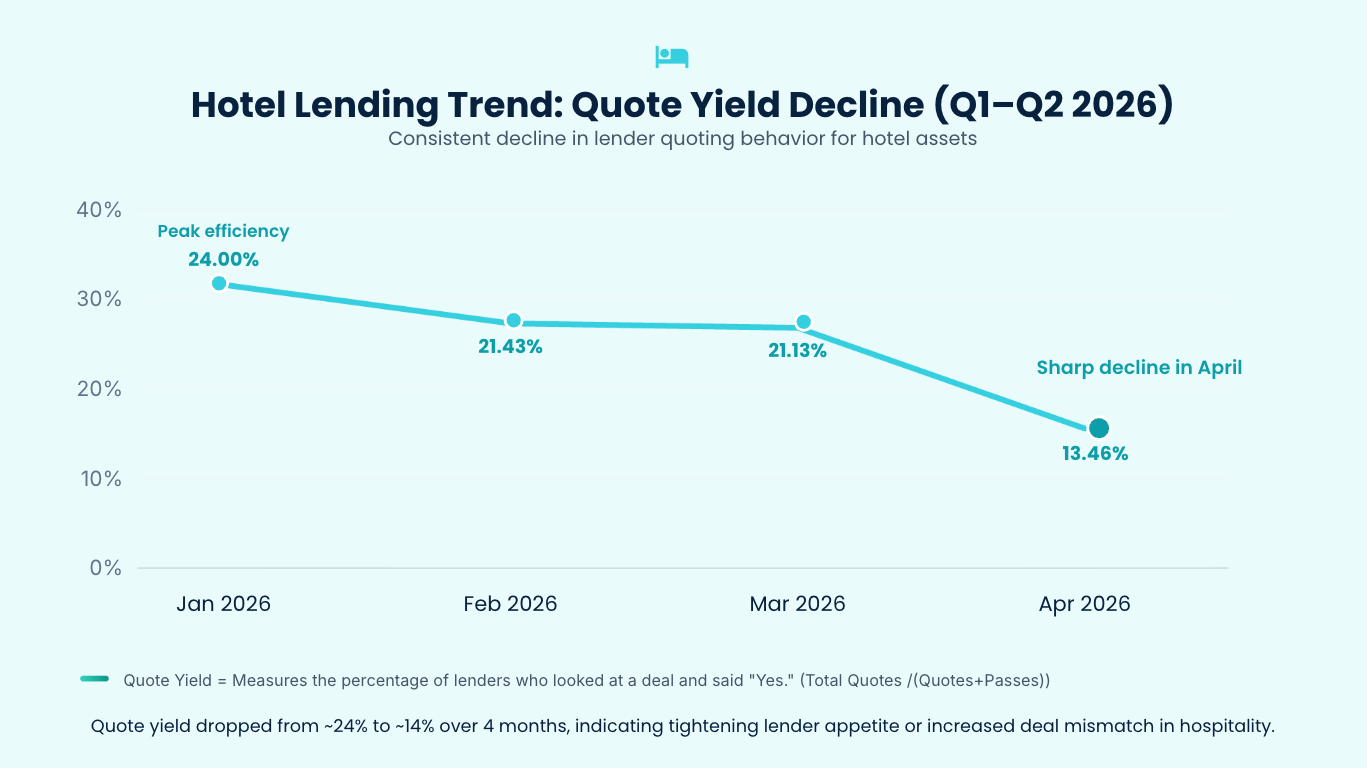

Hotel construction came in at a 13.89% quote yield rate in Q1 2026. Stabilized hotel was 23.76%. The overall LoanBase market average was 26.51%.

The gap is not random.

Most brokers who hear repeated passes on hotel ground-up construction, which LoanBase tracks as Hotel GUC, arrive at the same explanation: lenders have pulled back from hospitality. That read is too broad, and it leads to the wrong strategy. The data points to something more specific. Lenders are still engaging with hospitality. What they are declining is hotel construction execution risk. Those are not the same thing, and treating them as such means contacting the wrong lenders and collecting passes that were never going to go anywhere.

Hotel Construction vs. Stabilized Hotel: 13.1% vs. 23.8%

LoanBase analyzed lender reply data across Q1 and early Q2 2026. Hotel overall generated 231 negative responses and 58 positive responses, a 20.07% positive share across the full hotel segment.

Break it into construction and stabilized and the split becomes clear.

Stabilized hotel, what LoanBase tracks as hotel non-construction, ran at a 23.8% ratio of quotes to passes and a 23.2% positive share. Hotel construction came in at 13.9% conversion. On unique deals, hotel construction covered 9 deals with negative responses versus 6 with positive ones.

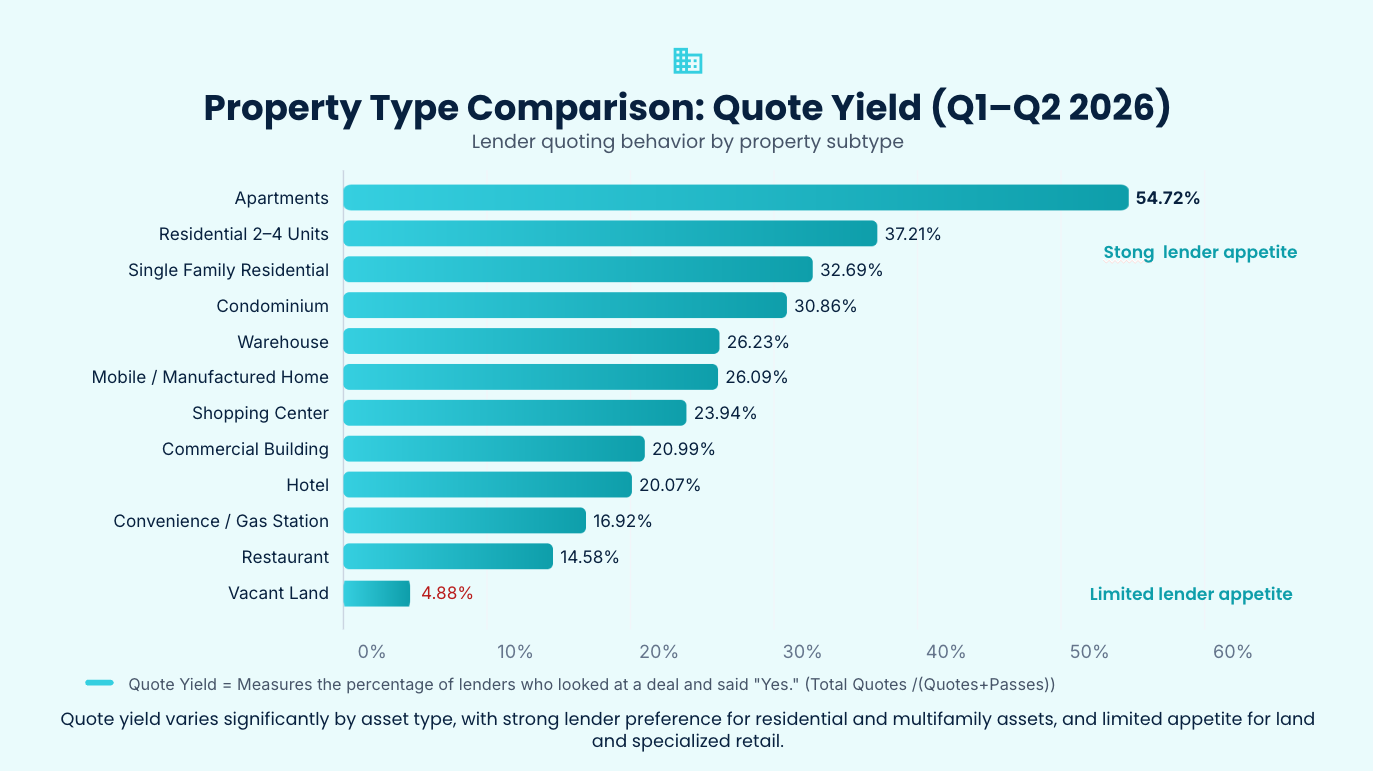

For reference, apartments hit 54.72% across the same period. Single-family residential came in at 32.69% Hotel construction ran at less than half the market average.

Hospitality is not the problem – construction is. Hotel construction is being treated as a different, more conditional risk bucket than hospitality overall, and lenders are making that distinction on every deal.

93 Passes. What Lenders Were Actually Saying.

The negative replies were not vague and they were not random. They came back around the same themes repeatedly.

Construction exposure was the most consistent blocker. “Too much construction for our fund.” “More construction than we’d want to do.” These were not lenders who had soured on hotels. They were lenders drawing a clear line at taking on a build. The hospitality appetite was there. The construction appetite was not.

Operating-only preferences came up deal after deal. “Operating hotels only.” “No land, development, or construction conversion.” Stabilized hotel deals were a different conversation for these lenders entirely. The screen was not the asset class. It was where the deal sat in the lifecycle.

Brand and flag requirements filtered out a significant slice of the remaining flow. “Only considering hotels with a major flag.” “For hospitality, we only fund limited service major flagged hotels.” Independent and unbranded hotel construction ran into this wall regardless of market or loan size.

Market caution showed up in some replies but as a secondary theme. The primary filters were construction exposure, operating status, and brand tier, not a broad rejection of travel-driven real estate.

$805 Billion in Projected Hotel Spending and Lenders Are Still Passing on Construction

The lender behavior in the data does not exist in isolation.

AHLA projects 2026 hotel guest spending to reach nearly $805 billion. STR and Tourism Economics still forecast slight improvement in overall U.S. hotel performance for the year. Hotel fundamentals are holding up.

But on the credit side, Trepp reported that in March 2026 the lodging CMBS delinquency rate saw the largest increase of any major property type. That is the number sitting on lenders’ desks when a new hotel construction deal comes across.

JLL’s 2026 hotel investment outlook reflects the same tension: stronger debt availability broadly, but banks still capping hotel construction leverage around 60%–65% LTC and requiring tighter structure. The market for stabilized hospitality and the market for hotel construction are operating on two different tracks right now. The data confirms it.

National Banks at 40.0%. Debt Funds at 12.4%. The Lender Type Breakdown.

The response data by lender type sharpens the picture further.

National banks showed a 40.0% positive ratio on hotel construction, the strongest of any lender type in the sample, though on low volume. Regional banks came in at 20%. Agency lenders returned 0%.

Debt funds drove the majority of hotel construction response volume and came in at 12.4%. They are the most active lender type in the space but among the most selective on execution risk. Available, but expensive and structured tightly. The brokers who got quotes from debt funds on hotel construction knew going in exactly what box their deal needed to fit.

The pattern across lender types is consistent. Hotel construction that cleared the screen in 2026 tended to be branded with a major flag, sized above most lenders’ minimum threshold, in a market with clear demand fundamentals, and structured closer to stabilized than true ground-up risk. Agency lenders and life insurance companies are effectively out of hotel construction at this point. The active lender set is narrower than most hospitality outreach lists assume, and knowing which category your deal belongs to before outreach begins changes the entire process.

What This Means Before Your Next Hotel Construction Deal Goes to Market

Marketing hotel construction as a hospitality deal puts it in front of the wrong lenders. The passes that come back are not about the property type. They are about construction exposure, flag requirements, execution risk, and deal size. Knowing that changes how you build the lender list.

The question is not which lenders do hospitality. It is which lenders will take on hotel construction risk at this brand tier, in this market, at this loan size. That is a shorter list. But it is the one that actually produces quotes.

The brands matter. The market matters. The structure matters. Each one is a filter most hospitality outreach lists are not built around.

The brokers getting quotes on hotel construction in 2026 are not sending broadly to every hospitality lender. They are going directly to the lenders still willing to take on construction risk, and they are arriving with a deal that already clears the flag, size, and market filters before the first call.

LoanBase tracks lender responses across thousands of deals each quarter, including the full hotel construction breakdown by lender type, pass reason, and response patterns. It shows exactly where lender appetite is and where it is not, before your next hotel construction deal goes to market.