Entering 2026, the commercial lending market is often described as “tight” or “uncertain.” Our platform data tells a more nuanced story. Lending is not slowing – it is becoming more selective, faster-moving, and increasingly segmented by capital source and asset quality.

This analysis is based on anonymized, consented activity from LoanBase’s Q4 2025 platform usage, reflecting real submission behavior, lender responses, and quote activity.

The dataset includes insights derived from over 2,800 anonymized lender–broker platform communications and approximately $1B in submitted deal volume, aggregated with full user consent.

Rather than relying on market sentiment, this report focuses on how brokers and lenders are actually behaving inside live transactions – without accessing or reading any private communications.

What emerges is not contraction – it’s redistribution.

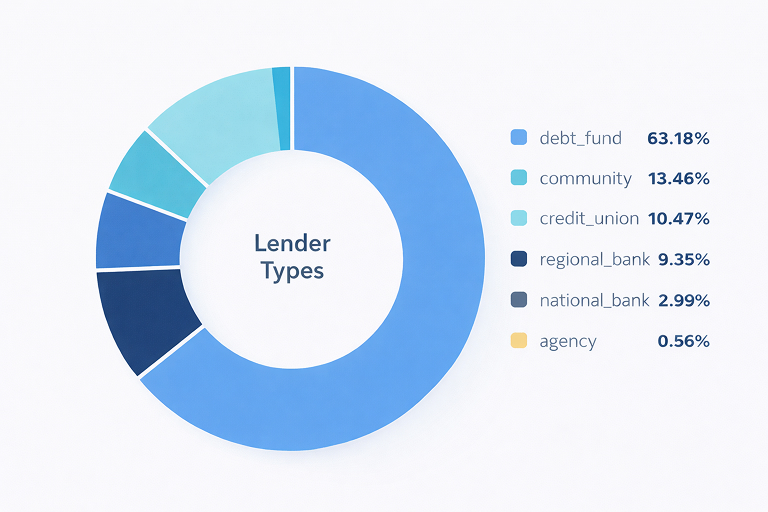

63% of Deals Flowed to Private Lenders

Private lenders have become the dominant execution channel.

In Q4 activity, over 63% of submitted deals were routed to debt funds and private lending groups, signaling a clear shift in how brokers are prioritizing capital sources. This is not simply about pricing. It reflects a market preference for speed, certainty, and flexibility.

Private lenders are closing deals roughly twice as fast as traditional institutions and converting opportunities at materially higher rates. Brokers are increasingly sequencing deals through private capital first to preserve momentum and de-risk timelines before exploring longer institutional processes.

Capital did not leave the market. It changed lanes.

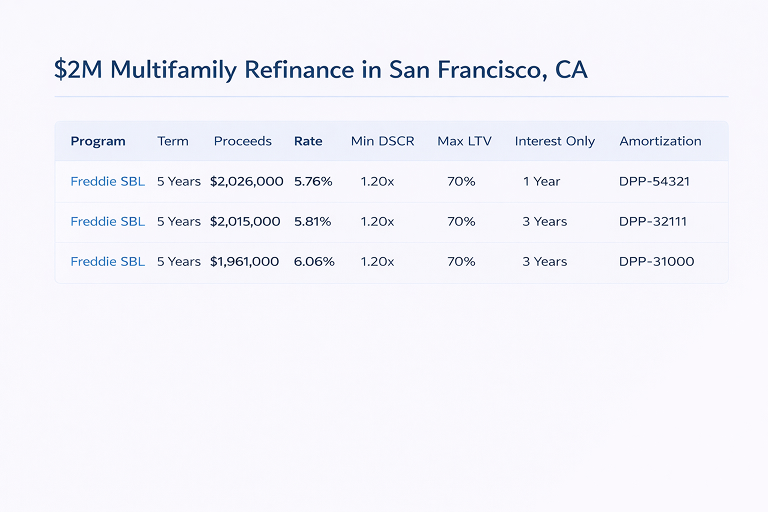

Agency Multifamily Rates Hovering Near 5%

While private lenders dominate deal velocity, agency lenders are setting the pricing floor.

Across stabilized multifamily transactions, agency executions are consistently anchoring rates near 5%, creating a renewed refinance incentive for borrowers who paused activity during peak rate volatility. As spreads compress, borrowers are re-entering the market and lenders are becoming more competitive across channels.

This dynamic is accelerating refinance pipelines and restoring deal flow that stalled during earlier uncertainty. For brokers, identifying agency-eligible assets early is once again becoming a leverage point when structuring borrower outreach.

Lower pricing is pulling volume back into the system.

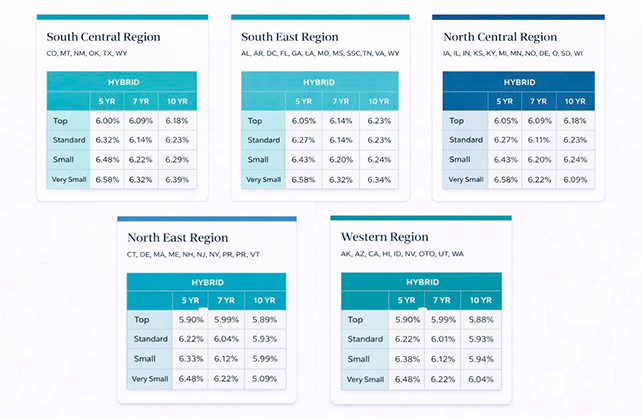

SBL Lowest Rates

Industrial Lending Activity Up Over 150%

Industrial lending is quietly becoming the fastest-growing CRE segment on the platform.

Comparing the most recent six-month period to the prior six months, industrial loan volume increased by more than 150%, accompanied by a similar rise in deal creation velocity. This growth reflects lender appetite for assets with stable tenant demand, operational simplicity, and predictable underwriting profiles.

While multifamily still dominates total market volume, industrial assets are emerging as one of the most efficient paths to lender engagement and execution speed.

For brokers, this is a category to watch closely heading into 2026.

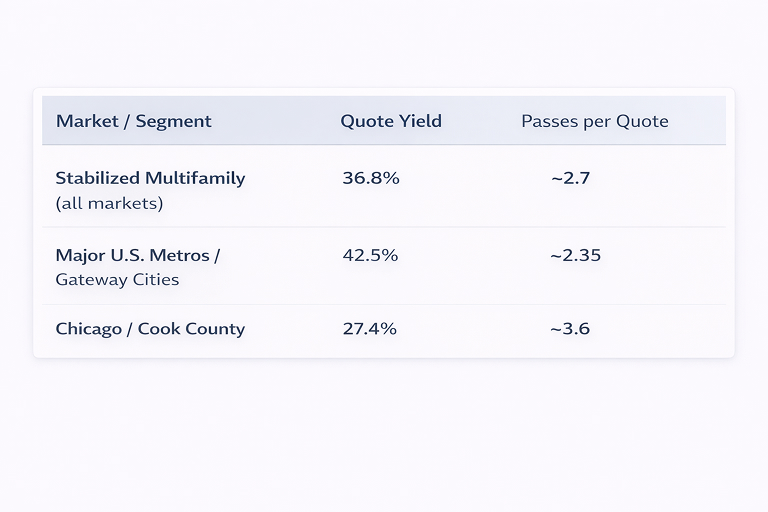

Chicago Quote Yield 27% vs 42% in Major Markets

Not all markets are being treated equally.

In Chicago and Cook County, lender quote yield sits near 27%, materially below the approximately 42% quote yield observed across major U.S. metro markets. This gap reflects increased underwriting friction tied to tax volatility, regulatory complexity, and longer legal timelines.

Deals in Chicago are not disappearing, but lenders are filtering more aggressively and selectively. Strong sponsorship, conservative leverage, and stabilized cash flow are increasingly required to generate competitive responses.

This is repricing behavior – not abandonment.

New York Multifamily Quote Yield Drops Below 16%

New York multifamily represents one of the clearest examples of structural tightening.

Platform activity shows a quote yield below 16%, significantly lower than national benchmarks. Lender hesitancy is particularly concentrated around assets located in core boroughs, where rent regulation exposure, expense inflation, and long-term valuation uncertainty remain persistent underwriting concerns.

Transactions still occur, but execution now depends heavily on asset quality, sponsor profile, and conservative deal structures.

In this environment, structure matters more than story.

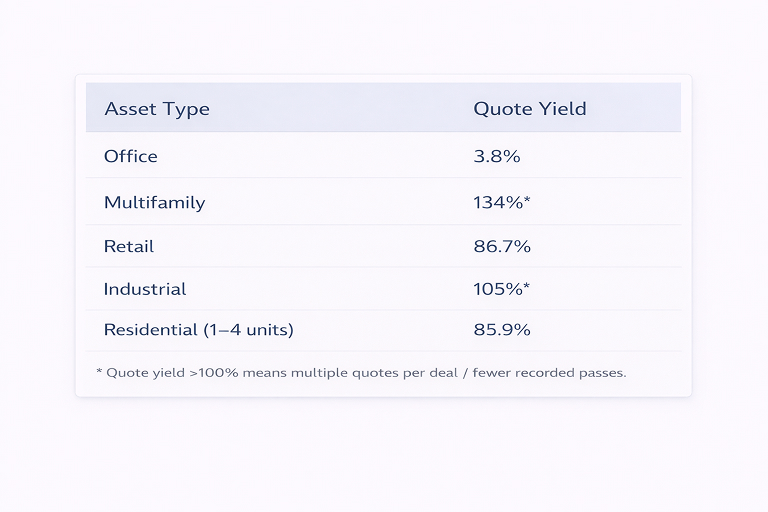

Office Lending Has the Lowest Quote Efficiency Entering 2026

Office remains the most consistently stressed asset class in CRE lending. LoanBase platform activity shows office-tagged deals receiving fewer lender quotes relative to submissions, with pass responses frequently citing valuation uncertainty, vacancy risk, and refinancing exposure.

When office deals do receive quotes, lenders often attach tighter leverage limits and higher DSCR thresholds – signaling risk repricing rather than standard execution. This pattern reflects broader market pressure. According to Trepp, office delinquencies remained the highest among major CRE asset classes entering 2026. At the same time, Reuters reports that regional banks continue reducing office exposure despite stabilization in other CRE sectors.

The takeaway is not that office capital is gone – but that underwriting paths are narrower, slower, and far more selective.

What This Means for Brokers Heading Into 2026

Across platform activity, top-performing brokers share similar operational patterns. They originate earlier in the deal lifecycle by focusing on maturing loan signals instead of cold outreach. They segment lenders by execution behavior rather than brand name. They prioritize structure before submission and track quote velocity as a real-time signal of deal health.

Most importantly, they are no longer reacting to capital availability. They are positioning ahead of it.

Market Outlook: Activity Is Accelerating, Not Contracting

Despite tighter underwriting in certain geographies and asset classes, overall platform behavior points toward acceleration.

Deal flow is increasing. Mid-market activity is rising. Private capital deployment is speeding up. Borrowers who paused decisions during rate volatility are returning as debt costs stabilize and spreads compress. Maturing loan volume continues to create sustained refinance demand.

At the same time, lenders are becoming more efficient, more competitive, and more responsive in qualified transactions.

The market is not freezing.

It is reorganizing around speed, data-driven origination, and execution certainty.

And that shift is reshaping how CRE deals will be sourced and closed in 2026.